Discover which nations let seniors use U.S. Medicare abroad, the type of coverage offered, and how to plan a safe medical tourism trip.

Read MoreU.S. Medicare – What You Need to Know

When talking about U.S. Medicare, a federal health‑coverage program for people 65+, certain younger disabled individuals, and those with End‑Stage Renal Disease. Also known as Medicare, it serves as the backbone of senior health insurance in the United States. A major option within the system is Medicare Advantage, a private‑plan alternative that bundles Part A, Part B and often prescription‑drug coverage. Another critical piece is Out‑of‑Pocket Costs, the expenses beneficiaries must pay for services Medicare doesn’t cover, such as deductibles, coinsurance, and certain specialist fees. Finally, Medical Tourism, the practice of traveling abroad for cheaper or faster procedures, often hinges on how much Medicare will pay and what gaps remain. Understanding these entities together helps you see why many patients compare domestic coverage with overseas options.

Key Concepts of Medicare

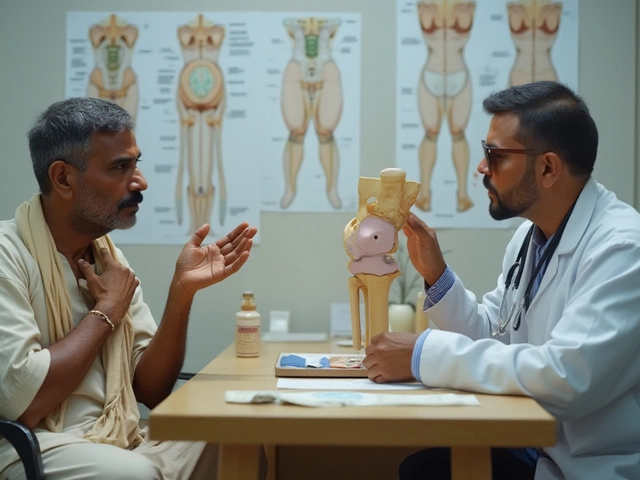

U.S. Medicare breaks down into four main parts. Part A covers inpatient hospital stays, skilled‑nursing facility care, and some home‑health services; it's usually premium‑free if you’ve paid Medicare taxes. Part B adds outpatient care, doctor visits, preventive services, and some medical supplies, charging a monthly premium that varies with income. Part C, or Medicare Advantage, lets private insurers offer a combined package that may include extra benefits like dental or vision. Part D supplies prescription‑drug coverage, also through private plans, with its own premium and a coverage gap called the “donut hole.” Eligibility starts at age 65, but younger people with certain disabilities or kidney disease qualify too. The program’s cost structure—premiums, deductibles, and coinsurance—creates out‑of‑pocket exposure that can be significant for high‑cost procedures. For instance, a knee replacement can trigger thousands in coinsurance, prompting some beneficiaries to explore medical tourism where the same surgery might cost a fraction. The decision to go abroad often depends on the balance between Medicare’s reimbursement limits and the patient’s willingness to manage travel, follow‑up care, and potential insurance gaps.

Below you’ll find a curated set of articles that dive into real‑world scenarios shaped by Medicare’s rules. From the hidden financial risks of delaying knee replacement surgery to state‑by‑state cost‑of‑living breakdowns that affect medical‑tourism choices, each post highlights how Medicare coverage—or the lack of it—impacts everyday health decisions. We also cover practical topics like picking safe herbal supplements, understanding diabetes medication alternatives, and navigating therapy timelines, all relevant when you’re weighing out‑of‑pocket expenses against possible savings. By reading on, you’ll gain actionable insights that help you make smarter choices about your health coverage, treatment options, and overall financial wellbeing under U.S. Medicare.

Which Countries Accept U.S. Medicare for Seniors?

Archive

Categories

Identifying Poor Candidates for Knee Replacement Surgery

Knee replacement surgery is a common procedure for alleviating chronic knee pain, but it isn't suitable for everyone. The surgery involves replacing damaged knee joints with artificial components, offering relief for many. However, certain individuals may face risks or complications that make them unsuitable for this procedure. This article explores who may not be an ideal candidate for knee replacement surgery, providing insights to help in making informed healthcare decisions.

Best Drinks for Easing Arthritis Symptoms

Living with arthritis can be a daily struggle, but the right drinks can ease the pain. This article dives into beverages that might help reduce inflammation and support joint health. From golden turmeric milk to tangy tart cherry juice, find out what could be soothing your aching joints. Hydration and inflammation-fighting drinks are key. Discover how simple daily choices can make a big difference.

Understanding the Painful Reality of Broken Bones: Which Hurts the Most?

Breaking a bone not only disrupts daily life but also brings intense pain. While some fractures are more notorious for their agony, such as femur or rib breaks, the severity can also depend on the person and circumstances. Factors such as nerve density, the bone's role in movement, and surrounding tissues contribute to the pain intensity. Exploring the various types of common fractures helps in comprehending which are among the most painful and why.

Who Should Avoid Using Ashwagandha?

Though ashwagandha is often hailed as a wonder herb in Ayurvedic medicine, it's not suitable for everyone. People should avoid it in certain situations, like during pregnancy, when experiencing certain medical conditions, or while taking specific medications. It's essential to know who should steer clear of this herb to prevent potential side effects. This article provides insights into who should use caution with ashwagandha and why.

The Highest Paid Doctor in Medical Tourism: Exploring Careers and Opportunities

The article delves into the highest earning professionals within the realm of medical tourism. It explores which medical specialists earn top dollar and why, focusing on the intricate mix of expertise, demand, and destination. The piece also provides insight into how the medical tourism industry is reshaping healthcare salaries and attracting talent worldwide. By examining case studies and examining the latest trends, this article offers a valuable perspective on the lucrative careers awaiting doctors in this burgeoning sector.